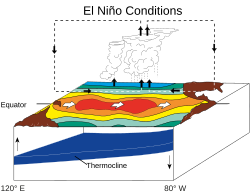

ENSO operates through shifts in sea surface temperatures and atmospheric pressure gradients across the equatorial Pacific. These shifts propagate through teleconnections that redistribute rainfall and temperature patterns globally. El Niño phases can produce drought in certain agricultural regions while increasing precipitation elsewhere. La Niña phases can intensify rainfall and flooding in the western Pacific.

Climate variability is not peripheral to real asset investing. It sits inside the operating core of agriculture, mining, and energy systems. The El Niño Southern Oscillation represents one of the most consequential climate oscillations influencing global production. It alters precipitation regimes, surface temperatures, wind circulation, and ocean dynamics across multiple continents. These changes affect crop yields, slope stability in open pit mines, tailings storage conditions, hydropower generation, transport corridors, and ultimately commodity pricing. For capital allocators in physical systems, ENSO is not an abstract climate index. It directly influences cash flow reliability and asset risk.

ENSO operates through shifts in sea surface temperatures and atmospheric pressure gradients across the equatorial Pacific. These shifts propagate through teleconnections that redistribute rainfall and temperature patterns globally. El Niño phases can produce drought in certain agricultural regions while increasing precipitation elsewhere. La Niña phases can intensify rainfall and flooding in the western Pacific while contributing to water scarcity in parts of South America. These are not isolated events. They influence planting cycles, harvest volumes, ore extraction rates, port access, energy load factors, and infrastructure resilience. The financial impact manifests through production volatility, operational disruptions, and widening spreads in commodity and sovereign markets.

Historically, climate driven volatility has been treated as an external shock absorbed through conservative underwriting or hedging strategies. What is changing is the capacity to integrate climate variability into structured probabilistic models. Advances in environmental data collection, remote sensing, and machine learning now allow atmospheric oscillations to be incorporated directly into yield forecasting, production modeling, and risk assessment. Sea surface temperature anomalies, wind field shifts, thermocline depth changes, and pressure differentials are quantifiable variables. When combined with localized agronomic, geological, and hydrological data, they form a predictive input set rather than a narrative explanation after the fact.

In agriculture, machine learning models trained on soil characteristics, historical rainfall, satellite vegetation indices, and ENSO phase indicators demonstrate measurable improvements in yield forecasting. The improvement does not remove uncertainty, but it narrows variance around expected output. In mining, rainfall intensity projections tied to ENSO phase probability can inform pit design parameters, drainage requirements, and slope stability assumptions. In energy systems, particularly hydro and wind assets, precipitation and wind regime modeling linked to oscillation cycles influence generation forecasts and maintenance planning. Across these sectors, the common thread is a transition from descriptive climate awareness to quantitative integration.

The financial implications are significant. When expected yield or production variance becomes narrower and empirically grounded, underwriting frameworks adjust. Business interruption assumptions become tied to modeled environmental exposure rather than historical averages alone. Debt covenants and capital structure decisions can incorporate scenario bands derived from climate probability distributions. Insurance pricing can differentiate between assets with similar commodity exposure but distinct environmental sensitivity profiles. Capital allocation shifts from broad sector views to asset specific environmental risk assessment.

The interaction between climate modeling and capital formation creates a feedback loop. Improved environmental modeling enhances production forecasts. Enhanced forecasts reduce perceived uncertainty. Reduced uncertainty improves financing terms and capital durability. Lower cost and more stable capital allows operators to invest in resilience infrastructure, which further reduces downside exposure. This process represents risk compression through information quality rather than risk elimination.

A platform operating across asset lifecycles can integrate this framework structurally. Development decisions can incorporate updated climate probability assessments at each stage gate. Transactional activity and offtake structuring can reflect expected volatility in output rather than static assumptions. Established operating businesses can continuously update forecasts as ENSO indicators evolve. Governance layers can maintain transparency by linking capital deployment to measurable environmental drivers.

Climate variability is expected to intensify as ocean heat content increases. ENSO phase shifts may become sharper or more frequent, amplifying production volatility in exposed regions. The appropriate response is not withdrawal from climate sensitive sectors, but improved modeling and structured integration. When atmospheric oscillations are embedded within financial analysis, real assets become more legible to capital. The transformation lies in converting environmental variability from an unpriced shock into a quantified underwriting input.

SKGP Strategic Partners

© 2026 SKGP Strategic Partners. All rights reserved. All proprietary frameworks, research, and materials are the intellectual property of SKGP Strategic Partners. Unauthorized use or distribution is prohibited.